12 Jun 2026

How Audit Trails Determine Profit Shares in Global Affiliate Payment Arrangements

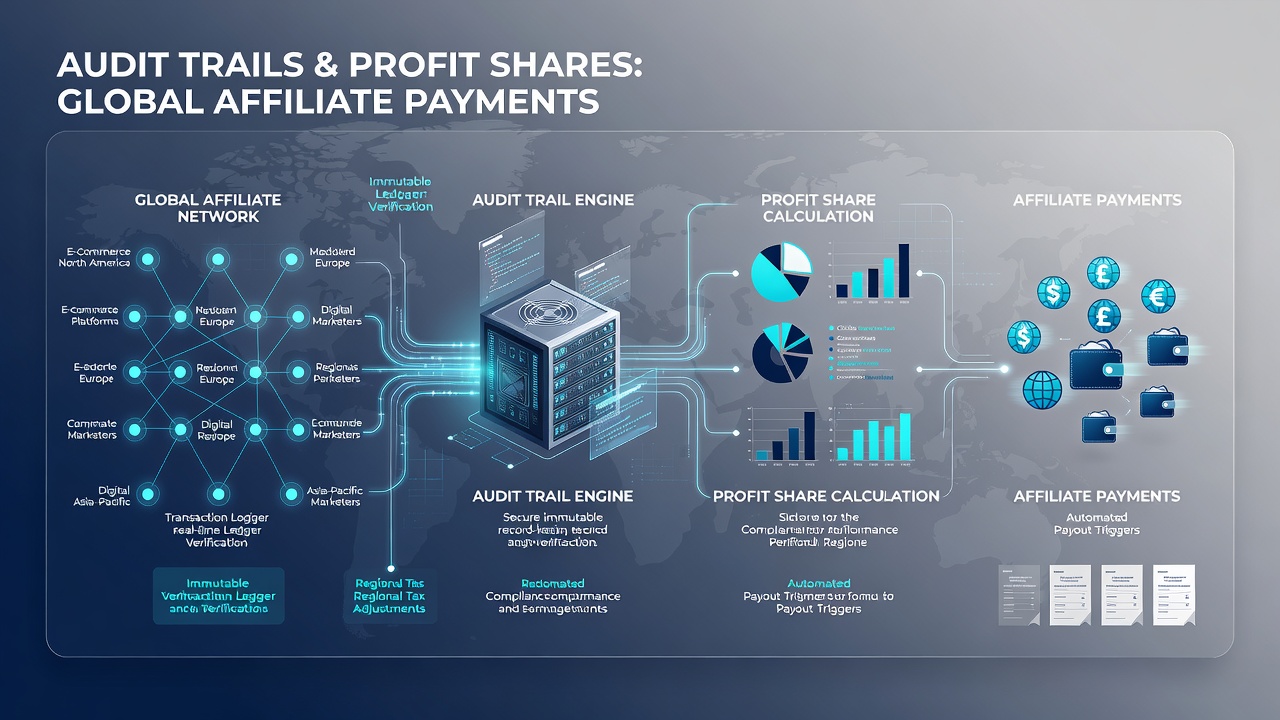

Audit trails function as detailed chronological records that capture every transaction, verification step, and data exchange within global affiliate payment arrangements, and these logs directly influence how profit shares get calculated and distributed among participating parties. Observers note that in systems spanning multiple jurisdictions, each entry timestamped and encrypted provides the raw data needed to confirm which affiliates drove specific merchant volumes or conversions. Research from the Bank for International Settlements indicates that cross-border payment volumes reached 190 trillion dollars annually by 2025, creating complex webs where audit trails prevent discrepancies in revenue splits.

Audit trails function as detailed chronological records that capture every transaction, verification step, and data exchange within global affiliate payment arrangements, and these logs directly influence how profit shares get calculated and distributed among participating parties. Observers note that in systems spanning multiple jurisdictions, each entry timestamped and encrypted provides the raw data needed to confirm which affiliates drove specific merchant volumes or conversions. Research from the Bank for International Settlements indicates that cross-border payment volumes reached 190 trillion dollars annually by 2025, creating complex webs where audit trails prevent discrepancies in revenue splits.Core Components of Audit Trails in Payment Networks

Transaction identifiers, user authentication events, and API call logs form the backbone of these trails, while each component gets stored in immutable formats that withstand regulatory scrutiny across regions. Data shows that when an affiliate refers a customer who completes a purchase, the trail records the originating click, the payment processor response, and the final settlement amount, allowing automated reconciliation engines to allocate percentages based on predefined agreements. Those who've examined these systems find that missing or incomplete entries often trigger manual reviews that delay payouts by weeks or months.

Security protocols such as blockchain-based hashing add another layer because they create verifiable chains that link one event to the next without room for retroactive alteration, and this matters in arrangements involving partners from the United States, Singapore, and the European Union simultaneously. Figures from the World Bank reveal that discrepancies in unaudited cross-border flows can exceed 4 percent of total transaction value, underscoring why detailed trails have become standard in contracts signed after 2024.

Mechanisms Linking Trails to Profit Allocation

Profit shares emerge from formulas that weigh verified contributions against total revenue pools, and audit trails supply the metrics that feed these calculations through integration with enterprise resource planning software. A single merchant transaction might generate fees split among the platform operator, the referring affiliate, and the acquiring bank, yet only entries confirmed by multiple validation points count toward each party's tally. Experts have observed that real-time dashboards pull from these logs to display running totals, enabling partners to monitor performance without waiting for monthly statements.

Dispute resolution relies heavily on these records because conflicting claims about referral sources get settled by cross-referencing timestamps and IP addresses against the original logs, and this process has grown more efficient since standardized API schemas gained adoption in 2025. One study from the University of Melbourne's Centre for Financial Studies highlighted that platforms using comprehensive trails resolved allocation disagreements 67 percent faster than those relying on summary reports alone.

Regulatory Influences and June 2026 Developments

Frameworks such as the European Union's revised Payment Services Directive and Australia's ePayments Code require retention of audit data for at least seven years, which directly shapes how long partners can contest profit distributions. In June 2026, updates to the Basel Committee guidelines on operational resilience are scheduled to take effect, mandating enhanced logging granularity for any arrangement exceeding 50 million euros in annual volume. Compliance teams have already begun adjusting their systems to meet these thresholds, ensuring that every fee adjustment and currency conversion remains traceable.

Geographic variations add complexity because rules in Canada emphasize consumer consent records within trails, whereas Singapore focuses on anti-money laundering flags that affect whether certain revenues enter shared pools at all. Partners operating across these markets must maintain parallel data structures to satisfy each authority without double-counting or omitting transactions that influence final shares.

Practical Examples from Existing Networks

Consider a scenario where an Asian-based affiliate promotes European merchants through a unified gateway; the trail captures the initial referral from a mobile app in Jakarta, the authorization processed in Frankfurt, and the settlement routed through a New York clearing house. Each step contributes data points that determine the affiliate's 12 percent cut versus the gateway's 3 percent service fee. Observers note that when volumes spike during seasonal campaigns, automated systems flag anomalies such as sudden referral clusters from single IP ranges, prompting deeper review before shares finalize.

Another case involves a North American processor collaborating with Latin American affiliates, where audit entries revealed duplicate claims on the same customer journey, resulting in reallocation of 2.3 million dollars across the network in early 2026. Such outcomes demonstrate how the presence of granular, cross-verified logs protects overall pool integrity and maintains trust among distant partners.

Conclusion

Audit trails continue to serve as the factual foundation for equitable profit distribution in global affiliate payment arrangements because they convert raw activity into auditable, shareable metrics that satisfy both contractual terms and regulatory demands. As volumes grow and rules evolve through 2026, the precision of these records determines whether allocations reflect actual contributions or require costly corrections. Partners who maintain robust logging practices position themselves to navigate increasingly interconnected systems with fewer interruptions to cash flow.